|

In a recent post, I wrote that capital expenditure (capex) spending, which includes the money allocated for building physical structures such as offices and manufacturing plants, is down, due in large part to uncertainty. That was a very blanket statement that doesn't apply to all companies. Take Amazon, for example. In the past five years, Amazon has spent $5.3 billion on capex, with $2.4 billion (43%) of that in the past 12 months.

So how, after such a painful economic downturn, can Amazon allocate so much money to capex? Simple: they have the cash and are using it wisely. Surely, Amazon is taking advantage of a soft construction market to stretch their capex dollars, of which they have $5.25 billion on their balance sheet. Know who else has a lot of cash on their balance sheets? Google ($16.3 billion) and Apple ($10.7 billion). Both of those companies are also investing heavily in capex. Apple had the best general contractors bidding for its proposed new campus. They get the benefit of high competition between reputable builders and relatively lower prices. The bottom line is that the market for commercial/industrial construction is tough, but there are some bright spots. In order to get that work, though, builders need to have a strong reputation to be invited to bid, meaning only a few will benefit from these capex expenditures.

2 Comments

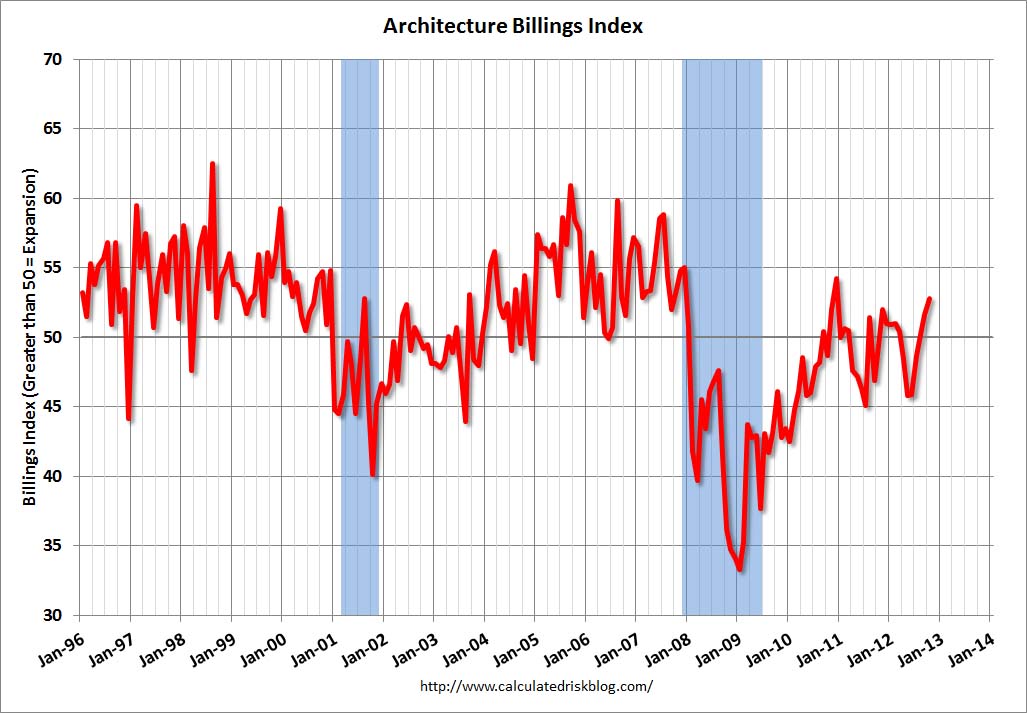

Architectural billings may be signalling a turn in the economy, but the gains are being localized is certain segments. Noted economist Nouriel Roubini tweeted today "Cash-strapped US consumers apparently cheery & spending while cash-rich US firms cutting sharply on capex [capital expenditures] spending & cautious on hiring." I think that summarizes the current market and builders need to be aware of that sentiment. Just before Thanksgiving, the American Institute of Architects (AIA) released their most recent Architecture Billing Index (ABI) figure. This measure is considered a leading indicator of non-residential construction by 9-12 months (and I'm assuming this means single-family home building is not included but multi-family housing is included since residential billings are a part of the measure). The October ABI score was reported as 52.8, up from 51.6 in September (measures over 50 signal increases in billings and measures under 50 signal decreases in billing). Even better, the October ABI for new projects was 59.4 versus 57.3 in September. Since design is *roughly* 10% of a building's cost, even modest increases in architectural billings can be leveraged into much larger amounts of money being allocated for building construction in the following months. If this is the case, these positive trends in ABI could reverse corporate America's reluctance to invest in capital expenditures like buildings and other facilities (as I discussed below on 11/20/2012--"Manic news for builders). ABI values over time can be seen in this figure created for the Calculated Risk blog (http://www.calculatedriskblog.com). The trend has been upward (albeit choppy) since January 2009:

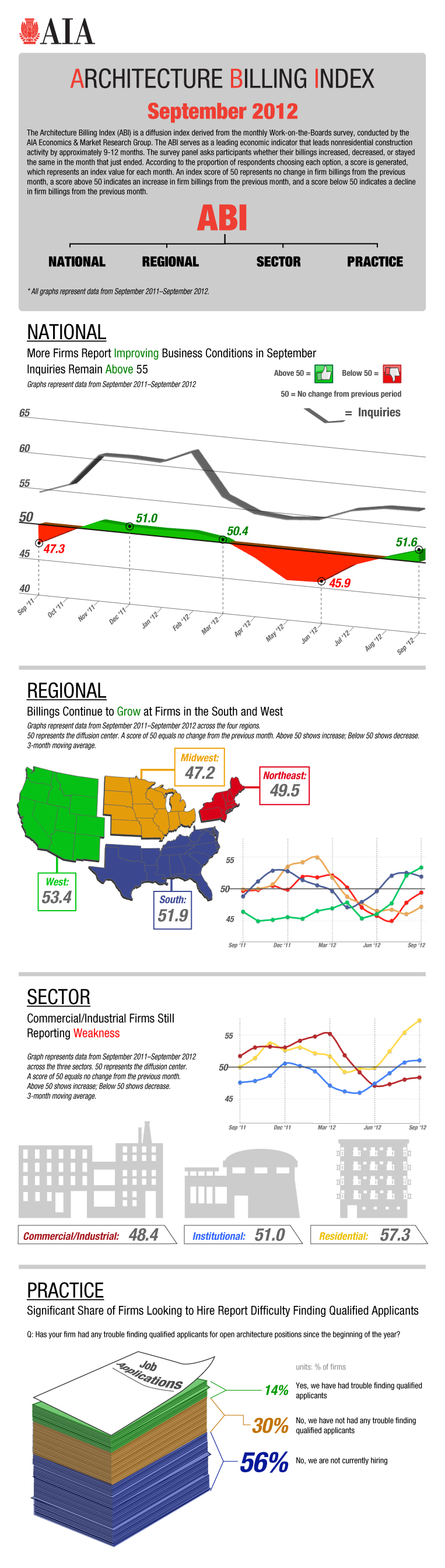

But like anything else the devil is in the details. Let's dig into the AIA's report, which can be read here but is nicely summarized in this figure produced by the AIA:  To access this figure, click here. The gains in ABI have been concentrated in the south (which has been growing faster than most regions in the U.S. for some time, relatively speaking) and the west (which was hit harder in the previous recession, again relatively speaking, and thus likely to see a bigger rebound). Also, the gains in ABI are due mostly to billings in residential, with some gains due to institutional (in northern California, hospital, prison, and university work seems to be the overwhelming majority of building construction, so this doesn't surprise me). (As a side note, it seems to me that institutional would likely follow housing, as schools and hospitals tend to be built as housing is built, but that's a very simple hunch on my part.) Commercial/industrial is a drag on ABI and this indicates there is decreasing amounts of this work in the pipeline for contractors.

There are some other things people need to be aware of. While these positive trends in ABI for residential, combined with recent bullish news coming from single-family home builders, is good news, it's contingent upon some trends that must be mentioned. First, much of the home buying is due to policies that are driving the cost of borrowing for a home down. With the Fed keeping rates low, mortgage rates are also low (a 30-year mortgage at 3.75%? Yes, that's really good for a borrower!) and quantitative easing injecting money into the economy, right now is a great time to buy a house, assuming you can qualify for a loan. Second, the housing market is being buoyed by $25-30 billion (yes, billion with a "b") in private equity investors buying homes with the intent to rent them (Barry Ritholtz states that this buying could be 20% of the current market in this video). Barry continues to point out two very important issues that will change the housing market for the worse if they occur: 1) if the U.S. falls back into a recession, all of those PE buyers will bail out of their housing positions and flood the market, which will cause the housing prices to drop. Secondly, if policymakers at the federal level (the President and Congress) choose to eliminate or cap interest mortgage deductions, the market for housing, whether it be for single- and/or multi-family homes, will drop like a stone. This second issue is unlikely, as mortgage deductions are very popular with voters and thus messing with them would be political arsenic for elected officials, but it's being contemplated as a measure for national debt reduction. The bottom line is that architectural billings are up, which is a good sign for the building industry, but the constructors need to be cautious. First, the gains in billings are in the housing (and, to a lesser extent, institutional) market sector, which is being driven by favorable macroeconomic factors that have a finite shelf life should the economy not see more wide-spread improvements. Secondly, businesses still seem reluctant to invest in capex such as buildings and industrial facilities. These two issues are, on some level, related (although it's way above my expertise to explain why). I'll feel a whole lot better if/when the commercial/industrial portion of the ABI measure improves. While still below the frothy levels of 2005 and 2006 (which is a good thing), the housing market seems to be making somewhat of a comeback. This sentiment is not based solely on today’s homerun report that there were 894k housing starts this month (above the forecast of 840k and more than the 872k last month). There’s actually several months of positive trends.

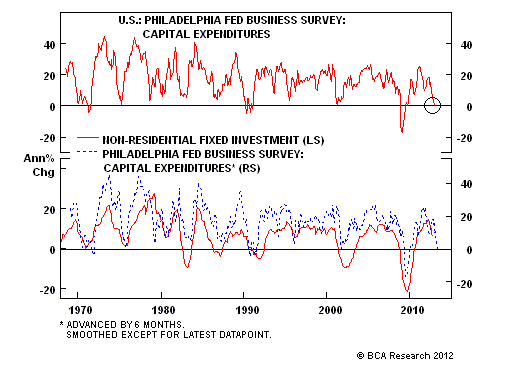

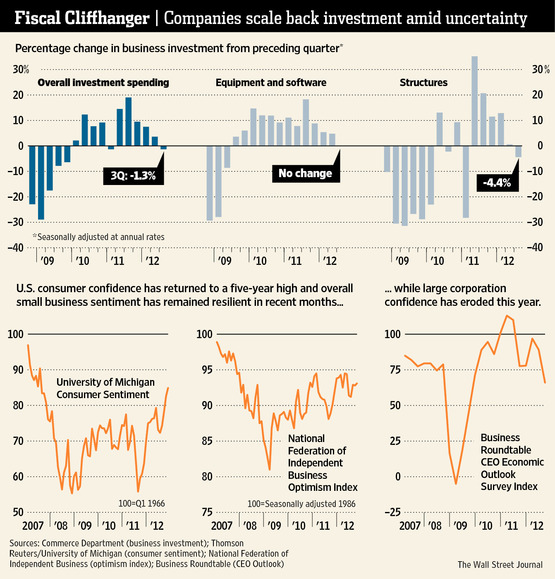

The housing market is not without its issues. Many people have been reducing their levels of household debt (deleveraging), although this great article by Joe Weisenthal presents the idea that a balance sheet recovery may be leading people to borrow money for housing. But for even those that want to buy, capital is still tight. Just because rates are low doesn’t mean that mortgages are easy to get. But with shrinking inventory and housing starts increasing, the news seems to be positive for homebuilders and, by extension, construction related to homebuilding. But what about private industry? Well, that’s a different story. Companies investing less in capital expenditures. Similar to families, companies are trying to reduce their debt levels and are decreasing the rate of investment in new facilities (or “non-residential fixed investments” in the figure below).

The better figure is the one below. It echoes the sentiment that companies are bearish on building structures, as investments are down 4.4% (see upper right graph in the figure below). A big reason for this pessimism: there is a general lack of confidence which may be the product of policy fear, market fear, regulatory fear, etc. Confidence is much higher than it was in 2009, but it’s trending downward in 2012 (see lower right graph in the figure below).

The bottom line is that homebuilding looks good, particularly in a market segment looking for good news, but commercial and industrial builders should still be cautious, as their corporate clients seem to be holding back on capital investments in structures.

|

Archives

January 2024

Categories |

RSS Feed

RSS Feed